Only a tenth away from mortgage money are from the base a few quintiles, which are the teams probably to spend

Financing Forgiveness try Improperly Geared to People that Have a tendency to Invest

Besides would financing termination provide apparently little spendable cash to help you houses, however the cash it does render could well be improperly targeted out-of a stimulus position.

Stimulus dollars that will be spent unlike protected offer a more powerful boost to help you near-label economic efficiency. Generally, those with low revenues otherwise who have educated previous negative income surprises are likely to blow most info. Yet , a big display of personal debt termination would go to men and women with higher income and those who features was able its earnings during the modern crisis.

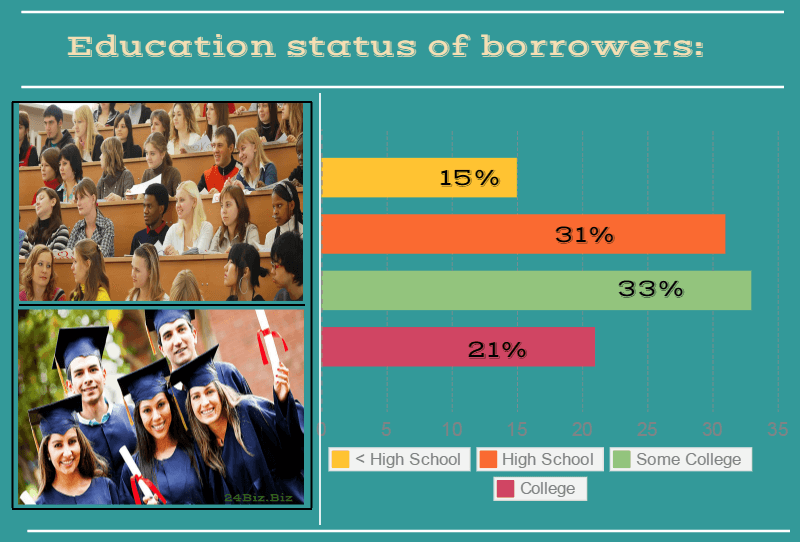

The majority of those really influenced by the modern financial crisis have likely little college student loans. More seventy percent of newest unemployed professionals don’t have a good bachelor’s studies, along with 43% exactly who failed to attend school after all. Meanwhile, lower than one to-third of the many scholar loans was held by households as opposed to a bachelor’s education much less than simply a tenth is held by people with no college education. Indeed, about a few-fifths of the many beginner personal debt was held by the households which have graduate grade. One category accounts for lower than a 10th of the full underemployed.

A recently available Pew survey also suggests that extremely financial struggling with the fresh pandemic is concentrated one of those having quicker knowledge for example quicker (if any) scholar loans.

Considering this information, it’s impractical that wide college student obligations termination is well-directed with the those sense income loss. Nor is it really targeted on the those with reduced profits. This new Brookings Institution recently estimated you to almost around three-household regarding student loan costs in certain (pre-pandemic) few days manufactured from the those in the major two quintiles.

The tiny  level of repayments from the reduced-money consumers is mostly due to the shipment away from financing themselves. But it’s also because people experiencing scholar obligations normally already benefit from lower costs lower than income-based cost programs or, for short-label income unexpected situations, pre-pandemic forbearance and you can deferment selection.

level of repayments from the reduced-money consumers is mostly due to the shipment away from financing themselves. But it’s also because people experiencing scholar obligations normally already benefit from lower costs lower than income-based cost programs or, for short-label income unexpected situations, pre-pandemic forbearance and you can deferment selection.

With forgiveness cash defectively aiimed at people going to invest – possibly based on money or money losings – the cash circulate deals so you’re able to borrowers was unlikely having an excellent large multiplier. CBO recently estimated the CARES Operate recuperation rebates – which provided $step 1,200 per adult and $500 for each boy to help you quite a few of family members while making lower than $150,100 a-year – had a beneficial multiplier away from 0.6x. Loan termination are substantially less targeted than just these rebates – which are already relatively untargeted – which means that tends to have a much down multiplier.

Targeting is some improved of the capping the level of mortgage forgiveness on, state, $50,one hundred thousand or $ten,one hundred thousand (as in President-choose Biden’s promotion bundle); or because of the focusing on because of the earnings, however, any style of loan termination goes simply to people with some amount of college education exactly who borrowed to have college. Therefore, actually a better directed adaptation is likely to be shorter stimulative than universal checks and much smaller stimulative than a great deal more targeted treatments such as prolonged unemployment masters.

Mortgage Forgiveness Enjoys a very Short Multiplier, and you will Similar Stimuli Was Offered from the a fraction of the new Costs

Assuming a 0.4x to 0.6x multiplier from additional cash flow from loan forgiveness, in combination with a 3 to 6 percent wealth effect, $1.5 trillion of debt relief might produce between $115 and $360 billion of economic output during the current downturn. 3 That suggests a multiplier of 0.08x to 0.23x.

These multipliers is actually far lower than simply any almost every other coverage already under consideration or passed from inside the present COVID save. Such, CBO estimated that present jobless benefit expansions had good multiplier regarding 0.67x and you can large recuperation rebates got a multiplier off 0.60x – both of that would end up being high in the future laws and regulations on account of smaller societal distancing.